Free Oregon It 1 Form

Oregon PDF Docs

Free Oregon It 1 Form

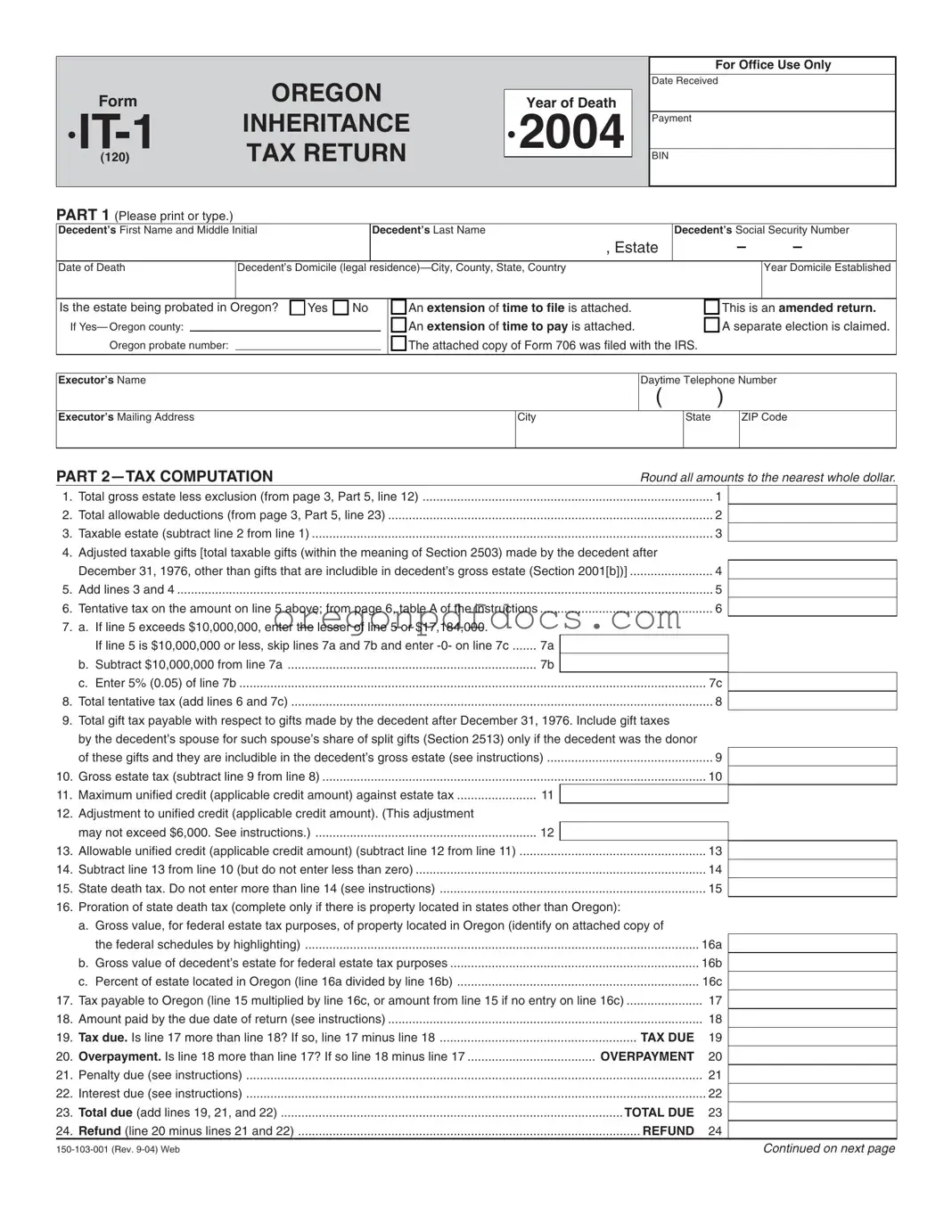

The Oregon IT-1 form plays a crucial role in the administration of estates in the state, particularly when it comes to the assessment of inheritance taxes. This form must be filed by the executor of an estate, and it requires detailed information about the decedent, including their name, Social Security number, and date of death. Additionally, it prompts the executor to disclose the decedent's domicile, which is essential for determining tax obligations. The form also includes sections for tax computation, where the executor calculates the taxable estate by considering gross estate values and allowable deductions. Specific questions regarding elections by the executor, such as whether to elect alternate valuation or special use valuation, are included to provide flexibility in tax reporting. Furthermore, the IT-1 requires the attachment of relevant documents, such as the death certificate, and it offers space to report on the marital status of the decedent and the benefits received by surviving family members. Overall, the Oregon IT-1 form is a comprehensive document that facilitates the estate settlement process while ensuring compliance with state tax laws.

Oregon IT-2 Form: Similar to the IT-1, the IT-2 is used for estate tax purposes in Oregon. It helps report the taxable estate and compute the tax due, similar to the calculations required on the IT-1.

Federal Form 706: This federal estate tax return is comparable to the IT-1 as it outlines the decedent's gross estate, deductions, and tax calculations. Both forms require detailed information about the estate's value and liabilities.

California Form 540: While primarily an income tax form, it shares the structure of reporting various income sources and deductions. Like the IT-1, it requires careful computation to determine tax obligations.

New York Estate Tax Return (Form ET-706): This form is similar in purpose to the IT-1, focusing on the estate's value and calculating the corresponding tax. Both forms require detailed financial information about the decedent's estate.

IRS Form 1040: Although it's an individual income tax return, it shares similarities in requiring detailed personal financial information. Both forms demand accuracy in reporting financial data.

Washington Estate Tax Return: This form serves a similar function as the IT-1, focusing on estate valuation and tax computation. Both forms necessitate comprehensive estate details for accurate tax assessments.

Illinois Estate Tax Return: Like the IT-1, this form is used to report estate values and calculate taxes owed. Both require detailed information about the decedent's assets and liabilities.

Texas Estate Tax Form: While Texas does not impose an estate tax, the form used for reporting is similar to the IT-1 in structure. It gathers information on the decedent's estate for record-keeping purposes.

Florida Estate Tax Return: This form, while not currently in use, historically served a similar purpose to the IT-1 by detailing estate values and tax computations for the state.

Virginia Estate Tax Return: This form is comparable to the IT-1 as it requires information about the estate's gross value and deductions to determine tax liability.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For Office Use Only |

||||||||

|

|

|

OREGON |

|

|

|

|

|

|

Date Received |

|||||||||||||||||||||

|

Form |

|

|

Year of Death |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

• |

INHERITANCE |

• 2004 |

|

|

Payment |

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

(120) |

|

TAX RETURN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

BIN |

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PART 1 (Please print or type.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Decedent’s First Name and Middle Initial |

|

|

|

|

Decedent’s Last Name |

|

|

|

|

|

|

Decedent’s Social Security Number |

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

, Estate |

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Date of Death |

Decedent’s Domicile (legal |

|

|

|

|

|

|

|

|

|

|

|

Year Domicile Established |

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

Is the estate being probated in Oregon? |

|

Yes |

|

No |

|

|

|

An extension of time to file is attached. |

|

|

|

|

|

|

This is an amended return. |

||||||||||||||||

If Yes— Oregon county: |

|

|

|

|

|

|

|

|

|

|

|

An extension of time to pay is attached. |

|

|

|

|

|

|

A separate election is claimed. |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

Oregon probate number: |

|

|

|

|

|

|

|

|

|

|

The attached copy of Form 706 was filed with the IRS. |

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Executor’s Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Daytime Telephone Number |

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

( |

|

|

|

) |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

Executor’s Mailing Address |

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

|

State |

|

|

|

|

ZIP Code |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

PART |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Round all amounts to the nearest whole dollar. |

||||||||||||||||

1. |

Total gross estate less exclusion (from page 3, Part 5, line 12) |

|

|

|

|

|

|

|

|

|

1 |

|

|

|

|

|

|

|

|||||||||||||

2. |

..............................................................................................Total allowable deductions (from page 3, Part 5, line 23) |

|

|

|

|

|

|

|

|

|

2 |

|

|

|

|

|

|

|

|||||||||||||

3. |

....................................................................................................................Taxable estate (subtract line 2 from line 1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

|

|

|

|

|

|

|

||||||

4. |

Adjusted taxable gifts [total taxable gifts (within the meaning of Section 2503) made by the decedent after |

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

........................December 31, 1976, other than gifts that are includible in decedent’s gross estate (Section 2001[b])] |

|

|

|

|

|

4 |

|

|

|

|

|

|

|

|||||||||||||||||

5. |

Add lines 3 and 4 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

|

|

|

|

|

|

|

|||

6. |

..................................................Tentative tax on the amount on line 5 above; from page 6, table A of the instructions |

|

|

|

|

|

6 |

|

|

|

|

|

|

|

|||||||||||||||||

7. |

a. If line 5 exceeds $10,000,000, enter the lesser of line 5 or $17,184,000. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

If line 5 is $10,000,000 or less, skip lines 7a and 7b and enter |

7a |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

b. Subtract $10,000,000 from line 7a |

|

|

|

|

|

|

|

|

|

|

7b |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

c. Enter 5% (0.05) of line 7b |

....................................................................................................................................... |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7c |

|

|

|

|

|

|

|

||||

8. |

Total tentative tax (add lines 6 and 7c) |

.......................................................................................................................... |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8 |

|

|

|

|

|

|

|

||||

9.Total gift tax payable with respect to gifts made by the decedent after December 31, 1976. Include gift taxes

by the decedent’s spouse for such spouse’s share of split gifts (Section 2513) only if the decedent was the donor

|

of these gifts and they are includible in the decedent’s gross estate (see instructions) |

9 |

|

|

10. |

Gross estate tax (subtract line 9 from line 8) |

10 |

|

|

.......................11. Maximum unified credit (applicable credit amount) against estate tax |

11 |

|

|

|

12. |

Adjustment to unified credit (applicable credit amount). (This adjustment |

|

|

|

|

may not exceed $6,000. See instructions.) |

12 |

|

|

13. |

Allowable unified credit (applicable credit amount) (subtract line 12 from line 11) |

13 |

|

|

14. |

Subtract line 13 from line 10 (but do not enter less than zero) |

14 |

|

|

15. |

State death tax. Do not enter more than line 14 (see instructions) |

15 |

|

|

16.Proration of state death tax (complete only if there is property located in states other than Oregon):

a. Gross value, for federal estate tax purposes, of property located in Oregon (identify on attached copy of

|

the federal schedules by highlighting) |

16a |

|

|

b. Gross value of decedent’s estate for federal estate tax purposes |

16b |

|

|

c. Percent of estate located in Oregon (line 16a divided by line 16b) |

16c |

|

17. |

Tax payable to Oregon (line 15 multiplied by line 16c, or amount from line 15 if no entry on line 16c) |

17 |

|

18. |

Amount paid by the due date of return (see instructions) |

18 |

|

19. |

Tax due. Is line 17 more than line 18? If so, line 17 minus line 18 |

TAX DUE |

19 |

20. |

Overpayment. Is line 18 more than line 17? If so line 18 minus line 17 |

OVERPAYMENT |

20 |

21. |

Penalty due (see instructions) |

21 |

|

22. |

Interest due (see instructions) |

22 |

|

23. |

Total due (add lines 19, 21, and 22) |

TOTAL DUE |

23 |

24. |

Refund (line 20 minus lines 21 and 22) |

REFUND |

24 |

Continued on next page |

Page |

Estate of: |

|

PART |

|

|

Check the “Yes” or “No” box for each question. See instructions on page 7. |

||

1. |

Do you elect alternate valuation? |

1. |

2. |

Do you elect special use valuation? If "Yes," you must complete and attach Schedule |

2. |

3. |

Do you elect to pay the taxes in installments as described in section 6166? If "Yes," you must attach additional information; |

|

|

see instructions on page 12 |

3. |

4. |

Do you elect to postpone the part of the taxes attributable to a reversionary or remainder of interest as described |

|

|

in section 6163? |

4. |

Yes

Yes

Yes

Yes

Yes

No

No

No

No

No

PART

1. Marital status of the decedent at time of death:

Married |

|

|

|||

Widow or widower— Name of deceased spouse: |

|

SSN of deceased spouse: |

|||

Date of death of deceased spouse: |

|

|

|

||

Single |

|

|

|||

Legally separated |

|

|

|||

|

|

|

|||

2.a. Surviving spouse’s name:

b.Surviving spouse’s Social Security number:

c.Amount received (see instructions on page 12):

3.Individuals (other than the surviving spouse), trusts, or other estates who receive benefits from the estate (do not include charitable beneficiaries shown in schedule O) (see instructions). For Privacy Act Notice (applicable to individual beneficiaries only), see the instructions for Form 1040.

Name of individual, trust, or estate receiving $5,000 or more

Identifying number

Relationship to decedent

Amount (see instructions)

All unascertainable beneficiaries and those who receive less than $5,000 |

...................................................................... |

Total |

3 |

Check the “Yes” or “No” box for each question.

4. |

Does the gross estate contain any section 2044 property [qualified terminable interest property (QTIP) from a prior gift or |

|

||

|

estate]? See instructions on page 12 |

4. |

||

5. |

a. Have federal gift tax returns ever been filed? |

5a. |

||

|

If "Yes," please attach copies of the returns, if available, and furnish the following information: |

|

||

|

b. Period(s) covered: |

|

c. Internal Revenue office(s) where filed: |

|

Yes

No

No

Yes

No

No

If you answer “Yes” to any of questions

6. a. |

Was there any insurance on the decedent’s life that is not included on the return as part of the gross estate? |

6a. |

b. |

Did the decedent own any insurance on the life of another that is not included in the gross estate? |

6b. |

7.Did the decedent at the time of death own any property as a joint tenant with right of survivorship in which (a) one or more of the other joint tenants was someone other than the decedent’s spouse, and (b) less than the full value of the property is

|

included on the return as part of the gross estate? If "Yes," you must complete and attach Schedule E |

7. |

8. |

Did the decedent, at the time of death, own any interest in a partnership or unincorporated business or any stock in an |

|

|

inactive or closely held corporation? |

8. |

9. |

Did the decedent make any transfer described in section 2035, 2036, 2037, or 2038 (see the instructions for Schedule G)? |

|

|

If “Yes,” you must complete and attach Schedule G |

9. |

10. Were there in existence at the time of the decedent’s death: |

|

|

|

a. Any trusts created by the decedent during his or her lifetime? |

10a. |

|

b. Any trusts not created by the decedent under which the decedent possessed any power, beneficial interest, or trusteeship? .... |

10b. |

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

No

No

No

No

No

No

No

No

No

No

No

Continued on next page |

Page |

Estate of: |

|

PART |

|

|

Check the “Yes” or “No” box for each question. |

||

11. Did the decedent ever possess, exercise, or release any general power of appointment? If “Yes,” you must complete and |

|

attach Schedule H |

11. |

12.Was the marital deduction computed under the transitional rule of Public Law

|

line 20, and note on line 20 “computation attached” |

12. |

13. |

Was the decedent, immediately before death, receiving an annuity described in the “General” paragraph of the instructions |

|

|

for Schedule I? If “Yes,” you must complete and attach Schedule I |

13. |

14. |

Was the decedent ever the beneficiary of a trust for which a deduction was claimed by the estate of a |

|

|

spouse under section 2056(b)(7) and which is not reported on this return? If “Yes,” attach an explanation |

14. |

Yes

Yes

Yes

Yes

No

No

No

No

PART |

|

Round all amounts to the nearest whole dollar. |

|||

|

Gross Estate |

|

Alternate Value |

|

Value at Date of Death |

1. |

Schedule |

1 |

|

|

|

2. |

Schedule |

2 |

|

|

|

3. |

Schedule |

3 |

|

|

|

4. |

Schedule |

4 |

|

|

|

5. |

Schedule |

5 |

|

|

|

6. |

Schedule |

6 |

|

|

|

7. |

Schedule |

7 |

|

|

|

8. |

Schedule |

8 |

|

|

|

9. |

Schedule |

9 |

|

|

|

10. |

Total gross estate (add lines 1 through 9) |

10 |

|

|

|

11. |

Schedule |

11 |

|

|

|

12. |

Total gross estate less exclusion (subtract line 11 from line 10). Enter here and |

|

|

|

|

|

on line 1 of part 2 |

12 |

|

|

|

|

Deductions |

|

|

|

Amount |

13. |

...........................Schedule |

13 |

|

||

14. |

Schedule |

|

14 |

|

|

15. |

Schedule |

|

15 |

|

|

16. |

Total of items 13 through 15 |

|

16 |

|

|

17. |

Allowable amount of deductions from item 16 (see instructions on page 13) |

|

17 |

|

|

18. |

Schedule |

|

18 |

|

|

19. |

Schedule |

|

19 |

|

|

20. |

Schedule |

|

20 |

|

|

21. |

Schedule |

|

21 |

|

|

22. |

Schedule |

|

22 |

|

|

23. |

.............................Total allowable deductions (add lines 17 through 22). Enter here and on page 1, part 2, line 2 |

23 |

|

||

PART 6

Under penalties of false swearing, I declare that I have examined this return, including accompanying schedules and statements. To the best of my knowledge and belief it is true, correct, and complete. If prepared by a person other than executor, this declaration is based on all information of which the preparer has any knowledge.

Signature of Executor

X

Title

Executor’s Social Security Number

Date

Signature of Executor

X

Title

Executor’s Social Security Number

Date

Check the box to authorize the following individual(s) to receive and provide confidential tax information relating to the decedent and the estate:

Check the box to authorize the following individual(s) to receive and provide confidential tax information relating to the decedent and the estate:

Name of Preparer

Title

Telephone Number

( )

Mailing Address

City

State

ZIP Code

PLEASE ATTACH A COMPLETE COPY OF YOUR FEDERAL FORM, SCHEDULES, AND SUPPORTING DOCUMENTS

Mail to: Oregon Department of Revenue, PO Box 14110, Salem OR

2553 - Employers are encouraged to designate individuals familiar with tax matters to enhance communication.

Wh-38 - Utilizing the WH-38 properly helps contractors avoid disputes related to wage payments.

For those looking to understand the nuances of property transfer, the Alabama bill of sale documentation is crucial. This form serves as an essential part of the sales process, ensuring that all involved parties are protected. For more information, refer to our guide on the thorough Alabama bill of sale form.

Oregon Mileage Tax - Oregon implements these filing rules to promote fair and equitable taxation for public road usage.

| Fact Name | Details |

|---|---|

| Form Purpose | The Oregon IT-1 form is used for reporting inheritance tax for estates in Oregon. |

| Governing Law | The form is governed by Oregon Revised Statutes (ORS) Chapter 118. |

| Filing Requirement | All estates in Oregon must file this form if the gross estate exceeds the exemption amount. |

| Executor Information | The form requires the executor's name, contact information, and address for communication. |

| Due Date | The IT-1 form is typically due nine months after the decedent's date of death. |

| Tax Computation | Taxable estate is calculated by subtracting allowable deductions from the total gross estate. |

| Unified Credit | The form allows for a unified credit against the estate tax, which reduces the tax liability. |

| Extensions | Extensions for filing or payment may be requested, but must be documented with the form. |

| Supplemental Documents | A death certificate and other supporting documents must be attached when submitting the form. |

| Amended Returns | If changes are needed, an amended return can be filed, indicating the amendments on the form. |

The Oregon IT-1 form is a crucial document for reporting inheritance taxes related to a decedent's estate. However, it is often accompanied by several other forms and documents that provide additional information or fulfill specific requirements. Below is a list of these documents, each serving a unique purpose in the estate administration process.

Each of these documents plays a vital role in ensuring that the estate is administered correctly and that all tax obligations are met. It is essential for executors and beneficiaries to be aware of these requirements to navigate the process smoothly.